Tariff drama, Trump’s speech, US-Iran talks

- Trump’s 10% global tariffs take effect

- US faces $175 billion problem

- Oil prices steady ahead of US-Iran talks

- Gold slips on profit taking ahead of Trump speech

A sense of caution gripped markets on Tuesday as investors grappled with renewed trade uncertainty, fears over AI disruption, and geopolitical risk.

European markets flashed red while US equities pointed to a shaky start amid fresh trade drama. After the Supreme Court ruled against Trump’s tariffs last Friday, he fought back, announcing new global tariffs of 10% - which were hiked to 15% over the weekend.

His new 10% global tariffs went into effect on Tuesday, with no official directive on the 15% rate.

Ultimately, this development has opened a can of worms with the US facing a $175 billion problem in tariff refunds and a deteriorating fiscal outlook. Even existing trade deals remain at risk with Trump warning partners not to “play games” after the EU moved to freeze their trade deal with the United States.

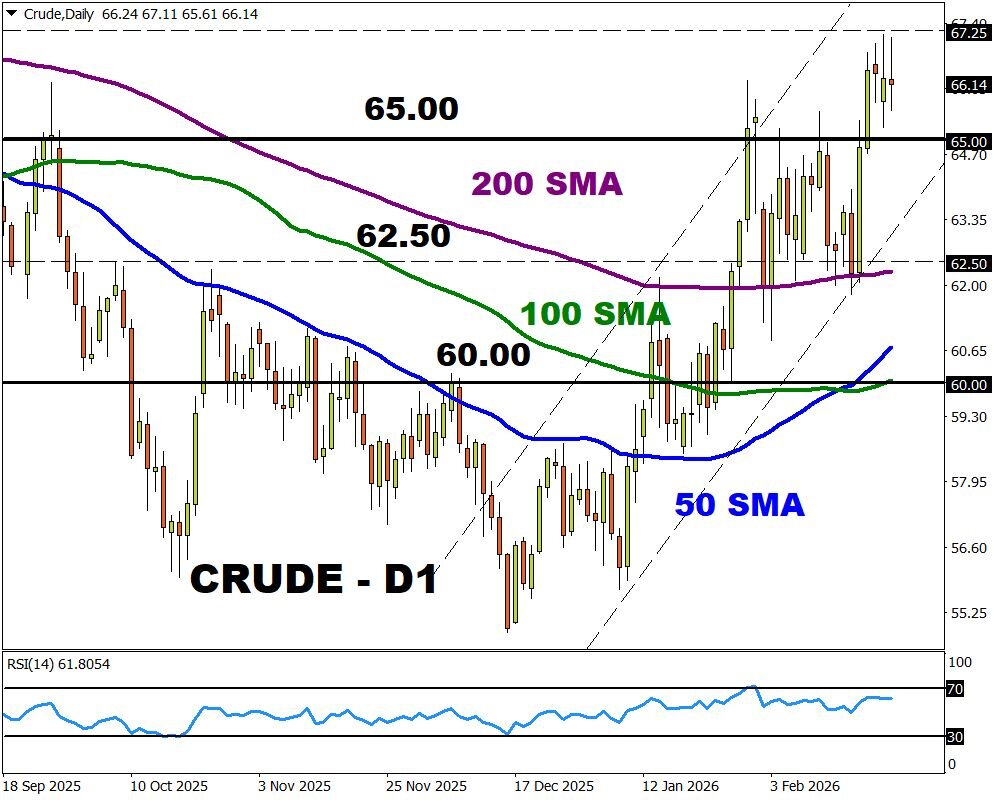

Oil steady ahead of US-Iran talks

Oil prices stabilised as diplomatic efforts eased fears of a major supply disruption.

Adding downward pressure, President Trump’s decision to raise global tariffs to 10% which may threaten future demand. The United States and Iran are to hold a third round of nuclear talks in Geneva on Thursday. Should the talks end on a positive note, leading to easing tensions, this could drag oil prices lower. However, the risk of any potential US military action could lead to a rapid upward reversal, keeping the Strait of Hormuz the primary market concern.

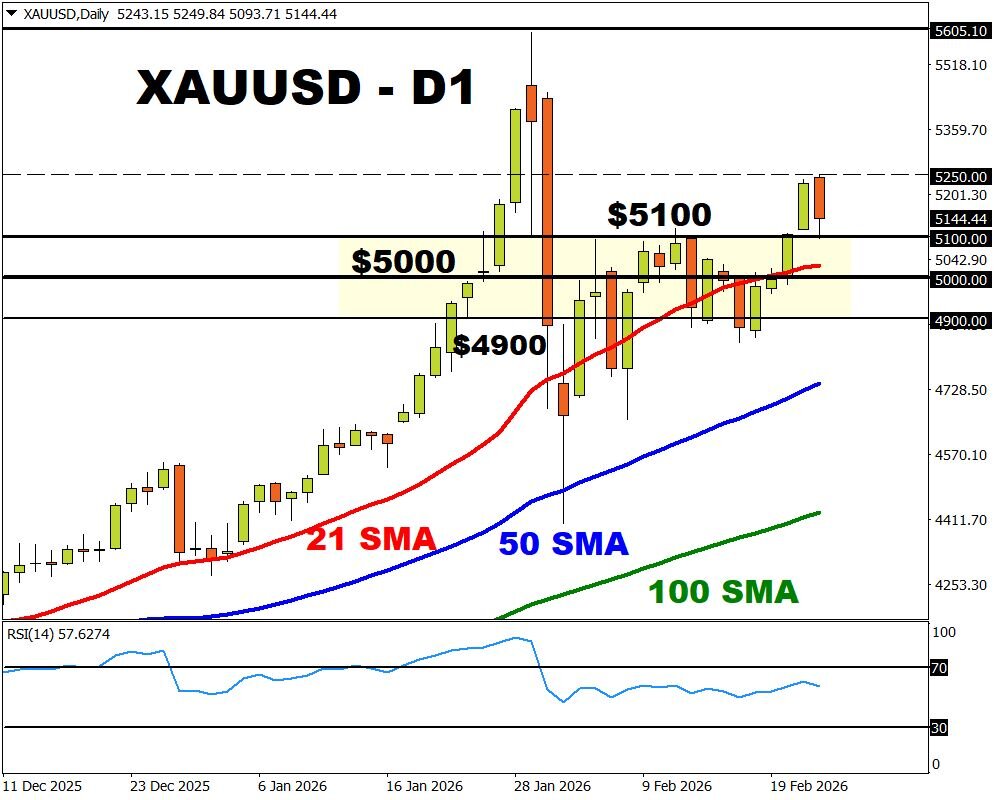

Commodity spotlight - Gold

Speaking of commodities, gold retreated as traders booked profits after four days of gains fuelled by risk aversion.

Although the precious metal is down over 1% today amid a stabilizing dollar, the fundamental forces powering gold bulls remain intact. Trump’s fresh tariff threats, geopolitical risk, and prospect of lower rates may limit gold’s downside pressure with major support at $5000.

Nevertheless, Trump’s State of the Union address, the outcome of US-Iran talks, Fed speeches and US data may influence the precious metals outlook this week.