Rate cut bets, US-Iran talks & US PCE in focus

- US/China markets closed for public holiday

- Markets on standby mode ahead of data packed week

- US-Iran talks in Geneva on Tuesday

- FX, commodity and crypto markets seek fresh catalyst

- Fed minutes + US PCE + US Q4 GDP = fresh volatility?

It’s a quiet start to another potentially busy week for markets.

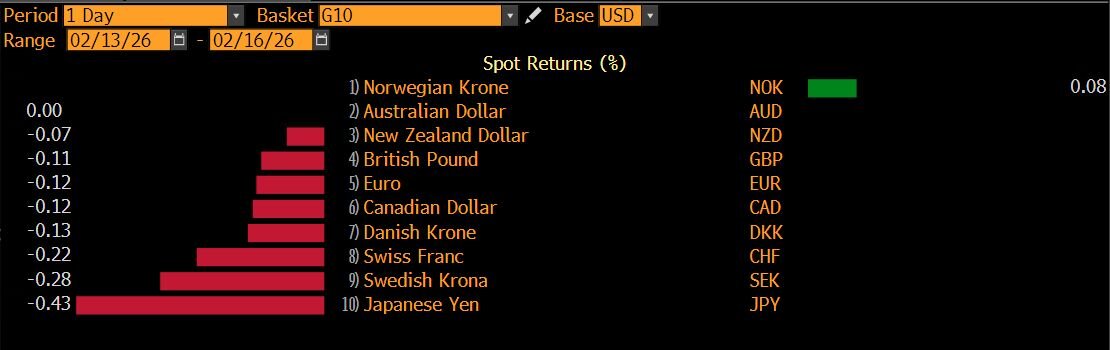

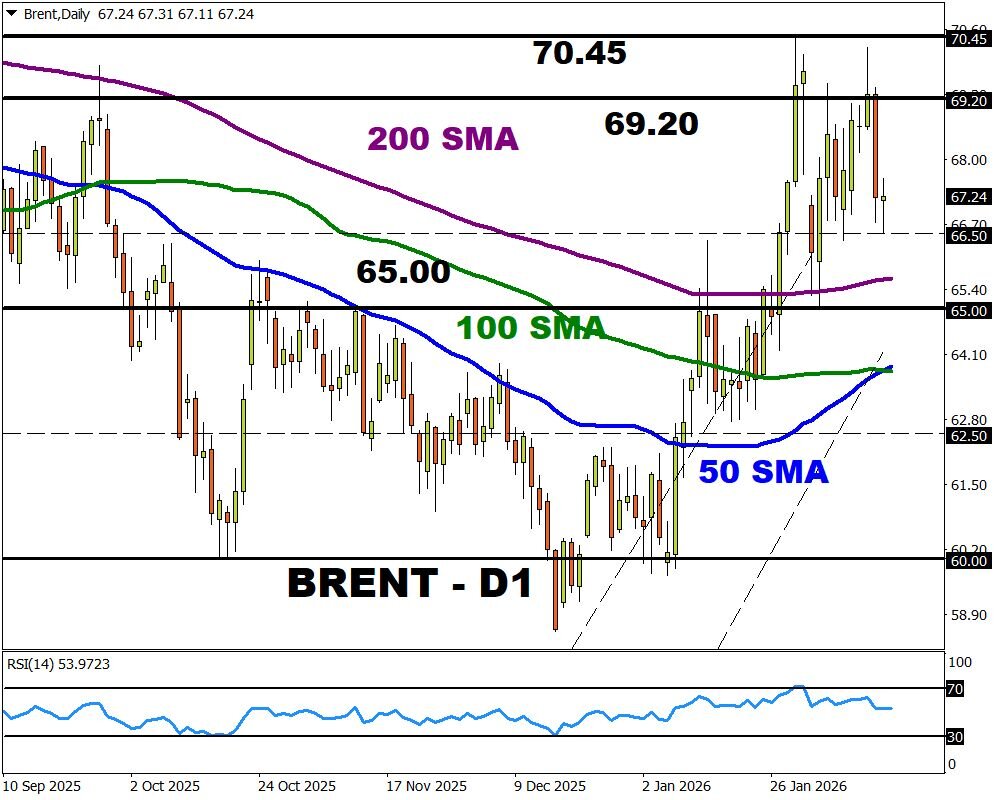

The dollar is rangebound, gold remains on standby, bitcoin lacks direction, while oil benchmarks are waiting for a fundamental spark.

US equity markets are closed on Monday for Presidents’ Day, while Chinese markets are closed all week due to the Lunar New Year holidays.

Nevertheless, things could spice up thanks to top-tier data and geopolitical developments.

On Tuesday, the US-Iran talks in Geneva may shape the near-term outlook for oil, which has gained over 10% year-to-date amid geopolitical risk.

Throughout the week, key data from Europe, the United Kingdom, Japan, and Australia may inject fresh life into global FX markets.

In the crypto space, Bitcoin is down over 20% year-to-date with prices currently hovering around the $70,000 level. Prices remain under pressure on the daily charts with $60,000 marked as a liquidation level, according to reports from Bloomberg.

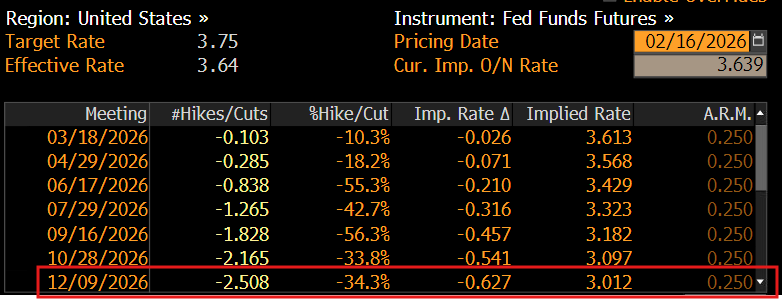

This week’s main event may be the Fed minutes, US PCE and the delayed US Q4 GDP report. The December PCE report will offer fresh insights into consumption while the GDP should provide insight into the health of the largest economy in the world.

Last Friday, the soft US CPI report supported the case for lower rates with traders pricing a 50% chance of a three Fed interest rate cuts in 2026.

Should the Fed’s preferred inflation gauge and latest GDP reinforce these dovish bets, this may deal another blow to the dollar while lending support to gold and US equities.

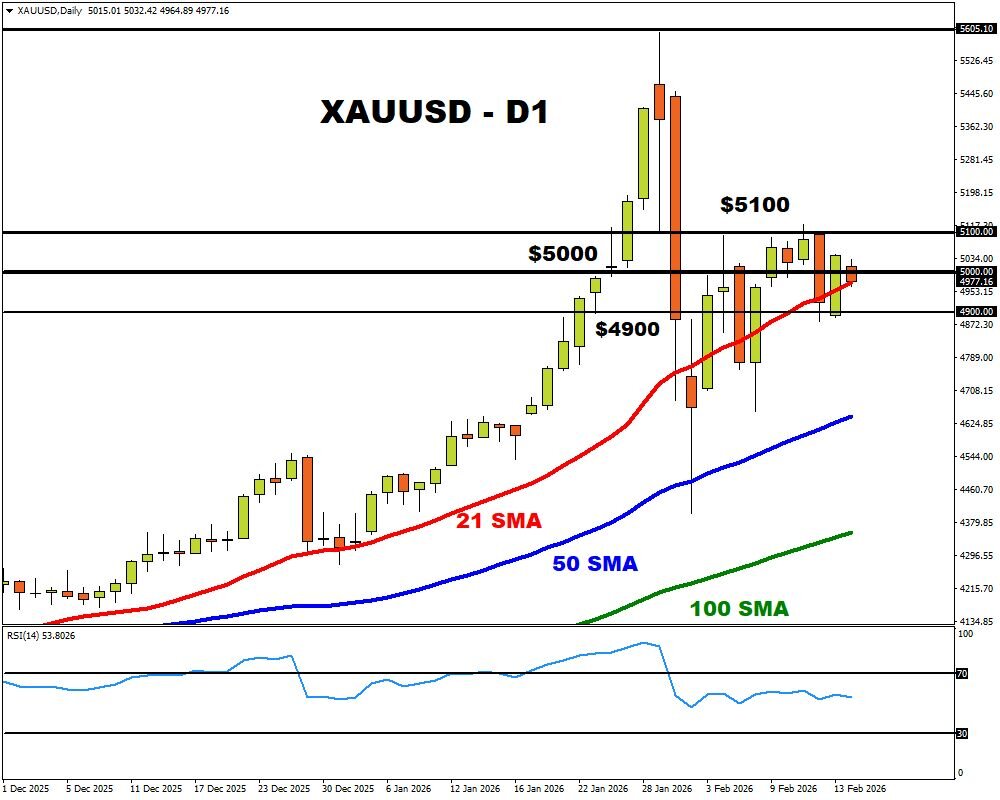

Speaking of gold, prices ended last week above the psychological $5000 level but has kicked off Monday on a timid note.

With markets in China closed this week, liquidity is likely to be thinner with geopolitics and US data driving prices. Should $5000 prove reliable support, gold may rally back toward $5100. However, weakness below $5000 could see a decline back toward $4880 and $4850.