Week In Review: Brent rallies, hawkish Fed minutes, US PCE in focus

- Mixed week for equities due to lack of catalyst

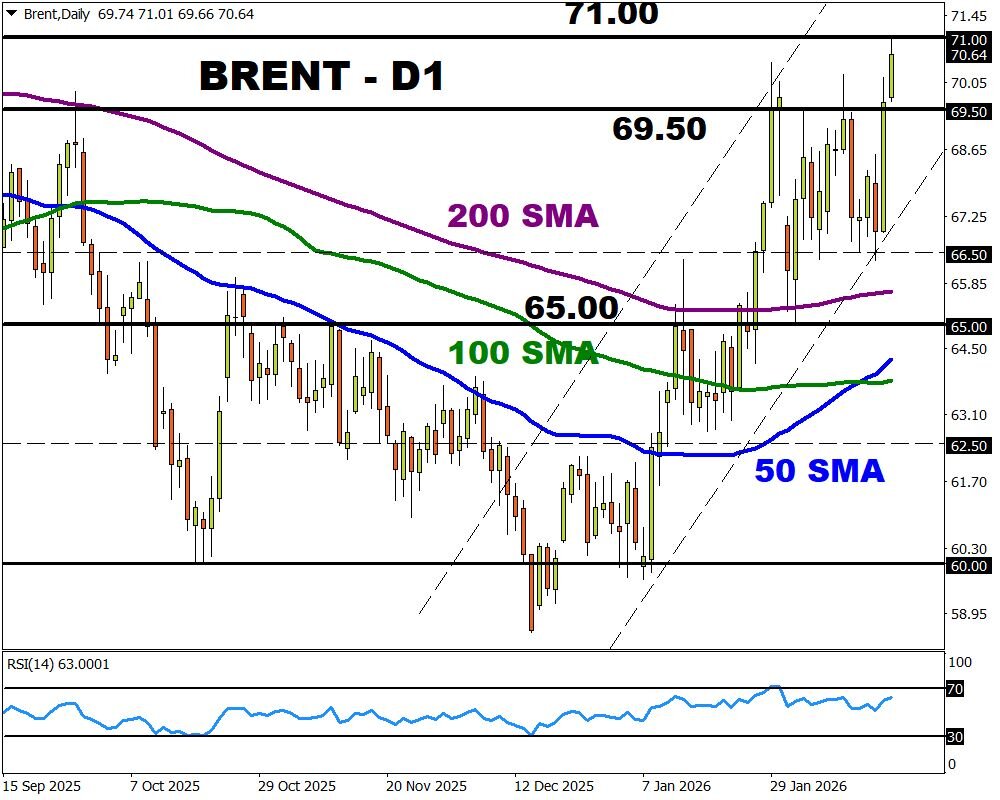

- Brent hits $71 on geopolitical risk

- Hawkish Fed minutes hit rate cut bets

- Gold on standby ahead of US PCE

It has been a relatively quiet week for markets due to the absence of any significant fundamental drivers.

US equities got off to a slow start due to the public holiday on Monday, while Chinese markets were closed all week thanks to the Lunar New Year. Lingering worries over the outlook for artificial intelligence promoted some volatility, but this was nothing special compared to previous weeks.

Yesterday evening, the Fed minutes showed several officials suggesting the central bank may need to raise rates if inflation remains stubbornly high. With only two dissenters favoring a cut and no indications of further easing, this shaved Fed cut bets for 2026.

Before the meeting, traders were pricing a 50% chance of three Fed cuts this year; this figure had dipped to under 30%.

In response, the dollar gained with FXTM’s DXY punching above 97.70.

Prices are turning bullish on the daily charts with a solid breakout above 98.00, opening a path toward the 200-day and 10-day SMA.

Looking at commodities, oil extended its biggest daily jump since October amid mounting geopolitical risk. Growing concerns around the US and Iran sinking deeper into a fresh conflict sparked fears around supply.

Brent touched $71 a barrel on Wednesday after rallying over 4% on Wednesday. Oil benchmarks have gained over 15% year-to-date, with the risk of conflict pushing prices higher.

Indeed, a potential war in the region that pumps about a third of the world’s oil could result in major supply disruptions – boosting oil prices.

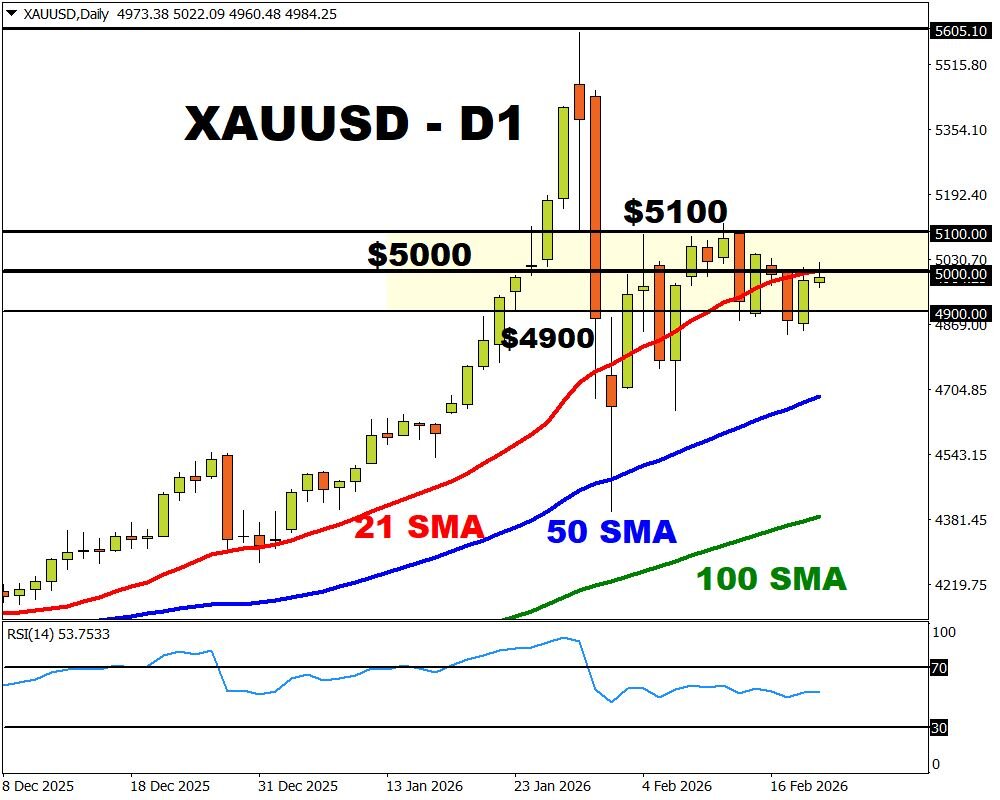

It’s been a flat week for gold with prices hovering around $5000. The precious metal seems to be waiting for the incoming US PCE/GDP combo which may shape Fed cut bets. A strong breakout above $5000 may open a path toward $5100. Weakness below $5000 could see prices test $4900.